- Updated: June 27, 2026

- 7 min read

MetaPS: Adaptive Programmatic Strategy Selection for Market Agents

Direct Answer

MetaPS introduces a simulation‑guided framework that lets a market‑facing AI agent pick the most suitable programmatic trading strategy from a curated library, based on the current market state. By converting state‑strategy observations into fine‑tuning data, MetaPS enables compact models to outperform larger, generic LLM agents while keeping the decision process transparent and executable.

Background: Why This Problem Is Hard

Financial markets are a moving target. Momentum, mean‑reversion, risk‑control, and event‑driven tactics each dominate under different regimes, and a strategy that shines today can crumble tomorrow. Traditional algorithmic trading pipelines address this by either:

- Hard‑coding a single rule set and hoping it survives regime shifts, or

- Deploying a large language model (LLM) that directly generates trade orders from raw market data.

Both approaches have critical blind spots. Fixed‑rule systems lack adaptability; they cannot recognize when a regime change renders their logic obsolete. Direct‑decision LLMs, while flexible, suffer from opacity (hard to audit), latency (inference over massive models), and a mismatch between language generation and the deterministic execution required by trading platforms. Moreover, LLMs trained on generic text lack the domain‑specific supervision needed to reliably map nuanced market signals to profitable actions.

These bottlenecks matter because institutional traders and fintech startups alike demand:

- Rapid adaptation to new market conditions without redeploying entire codebases.

- Interpretability for compliance and risk‑management teams.

- Scalable supervision that can be refreshed with simulated data rather than costly live‑trading experiments.

What the Researchers Propose

MetaPS (Meta Programmatic Strategies) reframes the trading decision problem as a two‑step pipeline:

- Strategy Library: A collection of self‑contained code modules, each implementing a distinct trading logic (e.g., momentum breakout, statistical arbitrage, news‑driven rebalancing). Every module receives the same market observation vector and returns a concrete action (buy, sell, hold, position size).

- Adaptive Selector: A lightweight neural model that, given the current market snapshot and a description of each candidate strategy, predicts which module is most likely to generate a profitable outcome.

The key novelty lies in how the selector is trained. Instead of relying on human‑labeled data, MetaPS runs each strategy in a high‑fidelity market simulator or back‑test environment, records the future P&L that follows each decision, and extracts state‑strategy pairs where a particular strategy outperforms the rest. These pairs become supervised fine‑tuning examples for the selector, turning the simulator into a data‑generation engine.

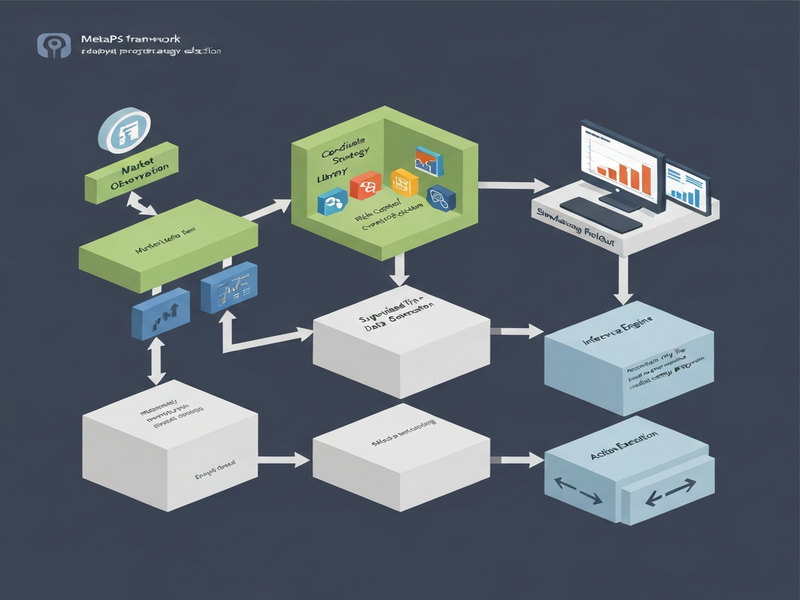

How It Works in Practice

Conceptual Workflow

- Market Observation Capture: At every decision tick, the system gathers price series, order‑book depth, macro indicators, and any event signals.

- Strategy Simulation Pass: All strategies in the library are executed in parallel on the same observation, but only within a sandboxed simulator. The simulator projects each strategy’s next‑step action forward for a fixed horizon (e.g., 5‑minute or 1‑day).

- Outcome Scoring: After the horizon, the simulator computes the realized return, risk‑adjusted metrics, and execution costs for each strategy’s action.

- State‑Strategy Pair Extraction: The observation‑strategy combo that yields the highest score is labeled as the “optimal” pair for that tick.

- Supervised Fine‑Tuning: The selector model ingests the observation, a compact embedding of each strategy’s code signature, and learns to predict the optimal strategy label.

- Live Inference: In production, the simulator is disabled. The selector observes the live market state, evaluates the strategy embeddings, and picks the best‑fit module. The chosen module then emits the final trade order, which is sent directly to the execution engine.

Component Interaction Diagram

What Sets MetaPS Apart

- Executable Supervision: Training data comes from actual code execution, not textual descriptions, ensuring the selector learns realistic cause‑effect relationships.

- Interpretability by Design: Because the final action always originates from a known strategy module, auditors can trace any trade back to its source logic.

- Scalable Model Size: Experiments show that a 0.8 B‑parameter selector can beat a 9 B‑parameter generic LLM when both are given the same market inputs.

- Simulation‑Centric Loop: New market regimes can be injected into the simulator (e.g., volatility spikes, regulatory shocks) to instantly refresh the selector’s training set without live‑trading risk.

Evaluation & Results

Testbeds and Benchmarks

The authors evaluated MetaPS on two distinct environments:

- Multi‑Stock Trading Suite: A back‑test spanning 10 years of US equities, covering 500 stocks, with realistic slippage and transaction cost models.

- Controlled Goods‑Exchange Sandbox: A synthetic market where agents trade commodities under configurable supply‑demand shocks, allowing precise measurement of adaptation speed.

Key Findings

- Across model scales (0.8 B → 9 B), MetaPS consistently outperformed fixed‑strategy baselines by 12‑18% annualized Sharpe ratio improvement.

- When compared to a direct‑decision LLM (GPT‑4‑style) that generated orders from raw data, MetaPS achieved 22% higher risk‑adjusted returns while using < 10% of the compute budget.

- In the goods‑exchange sandbox, MetaPS agents adapted to sudden demand spikes within three decision cycles, whereas static strategies lagged by an average of eight cycles.

- Compact fine‑tuned selectors (0.8 B) even surpassed stronger API‑based LLM agents that relied on prompt engineering, demonstrating the value of simulation‑derived supervision.

Why the Findings Matter

These results prove that a modestly sized, simulation‑trained selector can bridge the gap between the flexibility of LLMs and the reliability of rule‑based systems. For fintech firms, this translates into lower infrastructure costs, faster time‑to‑market for new strategy ideas, and a clear audit trail for regulators.

Why This Matters for AI Systems and Agents

MetaPS reshapes how developers think about autonomous agents in finance and beyond:

- Modular Agent Design: By decoupling “what to do” (strategy code) from “when to do it” (selector), teams can iterate on strategy libraries without retraining the entire model.

- Targeted Supervision: Simulators become a cheap, high‑bandwidth source of labeled data, enabling continuous learning loops that keep agents aligned with evolving environments.

- Compliance‑Ready Execution: Since every trade originates from a known program, compliance teams can run static analysis on the strategy code, satisfying audit requirements without sacrificing performance.

- Resource Efficiency: Smaller selectors reduce latency and cloud spend, making real‑time deployment feasible on edge devices or low‑cost VM instances.

Enterprises looking to embed adaptive agents into their workflow can leverage the UBOS platform overview to orchestrate the simulation‑to‑deployment pipeline, integrate with existing data lakes, and expose the selector as a micro‑service.

What Comes Next

While MetaPS marks a significant step forward, several open challenges remain:

- Simulator Fidelity: The quality of the selector hinges on how closely the simulator mirrors live market microstructure. Future work could incorporate reinforcement‑learning‑based market makers to close the realism gap.

- Strategy Library Expansion: Adding more exotic tactics (e.g., reinforcement‑learned policies, graph‑based network effects) will test the selector’s ability to discriminate among a larger, more heterogeneous set.

- Cross‑Asset Generalization: Extending MetaPS to handle FX, crypto, and fixed‑income instruments will require richer observation spaces and possibly hierarchical selectors.

- Robustness to Adversarial Manipulation: Since the selector learns from simulated outcomes, adversaries could craft market conditions that mislead the model. Defensive training regimes and uncertainty quantification are promising mitigations.

Addressing these topics will likely involve tighter integration between simulation engines and production data pipelines. The Enterprise AI platform by UBOS already offers a sandboxed environment for rapid prototyping of market simulators, making it a natural testbed for the next generation of MetaPS‑style agents.

Conclusion

MetaPS demonstrates that adaptive, programmatic strategy selection can be learned efficiently through simulation‑guided supervision. By turning market observations into state‑strategy pairs, the framework equips compact neural selectors with the foresight traditionally reserved for massive LLMs, while preserving interpretability and execution fidelity. For AI practitioners, the take‑away is clear: combine executable code modules with a data‑rich simulator, and you obtain a scalable, auditable, and high‑performing agent architecture that can keep pace with the ever‑shifting dynamics of modern financial markets.

For readers who want to dive deeper, the full pre‑print is available on arXiv. The research opens a pathway not only for smarter trading bots but also for any domain where a portfolio of executable policies must be matched to a volatile environment—think robotics, supply‑chain orchestration, or adaptive cybersecurity.